Purchasing Real Estate with Seller Financing

In a declining capital markets environment, owner financing can be the solution to completing a real estate transaction. Seller financing isn’t as common as traditional mortgages but can be a nice carrot in a high-interest-rate environment.

This blog post will discuss several different seller financing scenarios and show how they can be worked into the Tactica proforma models.

Contents

Owner Financing Primer

The vast majority of real estate is purchased with a combination of:

Cash (down payment)

In the rising interest rate environment, traditional loans are more expensive (due to higher interest rates) and have smaller allocations (less leverage), and some financial institutions have stopped underwriting altogether.

Projects that used to be a shoo-in for conventional funding may not qualify any more, and it could be up to the seller to keep skin in the game via a few types of seller financing (sometimes referred to as a purchase money mortgage).

100% Seller Financing: The seller finances the property for the buyer/borrower and assumes the role of the “traditional mortgage lender.”

Partial Seller Financing: The buyer gets the 1st mortgage loan, and the seller provides a subordinate second mortgage to help close the equity gap.

Partial Assumable Seller Financing: The buyer assumes the existing mortgage, and the seller provides a subordinate second mortgage to help close the equity gap.

Seller Financing Arrangement Benefits

The most significant benefit of seller financing from the buyer’s and seller’s perspective is that it could save the deal or allow the buyer to bring less cash to the closing table.

If the seller is financing 100% of the agreed-upon purchase price, there’d also be a ton of flexibility in terms of:

Monthly payments

Balloon payment dates

Closing costs

There is less focus on credit checks and credit scores that a traditional lender would undoubtedly factor

Deferring a portion of sellers’ capital gains (potentially)

Buyer non-recourse (as the property would be the collateral backing the note if the buyer defaults)

If the seller financing acts as a second mortgage, the buyer’s cash requirement will be less. If all goes well with the project, the buyer will likely refinance or sell the asset and make a full repayment to pay the seller’s loan, which could be a win-win for all parties involved.

Second Mortgage Cautions

If you purchase a property using a first-position mortgage and intend to pursue a second mortgage with the seller, it’s essential to ensure your lender allows it. Well-known lenders like Fannie Mae/Freddie Mac and CMBS generally don’t let a second-position mortgage. Taking out a second mortgage could lead to potential legal action from the 1st mortgage lender and foreclosure.

More exotic lenders, like banks, bridge lenders, or hard money lenders, may check off on a second mortgage, but verifying eligibility is essential. I talked to a banker recently who would allow a promissory note behind the first mortgage but won’t allow the seller to file a second mortgage.

Disclaimer: Verify the rules with your banker and a competent real estate attorney who can help you navigate the debt documents and purchase agreement stipulating the seller financing agreements.

Underwriting Seller Financing

The remainder of the article will cover several different seller financing scenarios and teach you how it works in Tactica’s Value Add Model and our Free Multifamily Template.

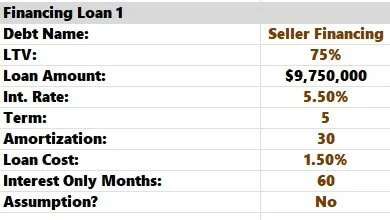

100% Seller Financing

If the seller is willing to finance a large enough chunk of the purchase price and you don’t need a mortgage, the financial model will make the inputs straightforward. You will treat the terms with the seller like a traditional mortgage. For example, if the seller were willing to finance 75% of the purchase price at 5.5%, 5-year term, full-term interest-only, you’d input:

We won’t need to worry about this scenario's “Loan 2” inputs.

Note: In negotiations with the seller, you could use the amortization assumption to skew the payment to more principal or interest.

Higher Amortization = More interest (but smaller total monthly payments)

Lower Amortization = Less interest (but higher total monthly payments)

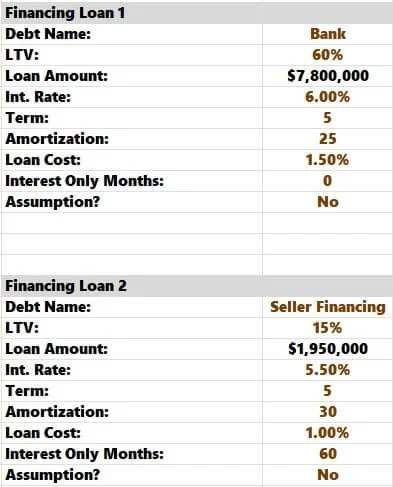

Partial Seller Financing

In this scenario, you found a local bank willing to give you a 60% LTV loan on the purchase price. However, you need the seller to carry another 15% of the purchase price because your cash is limited to 25% of the purchase price. The bank is okay with a seller carryback.

The capital stack is:

First Mortgage: 60%

Second Mortgage: 15%

Upfront Cash: 25%

First, you can check “Yes” for both financing options in the model.

Then enter the bank’s and seller’s loan terms.

The bank’s loan terms will amortize over 25 years, while the seller financing is interest-only. It’s important to mention that the “Loan 2” option is also a great spot to input supplemental loans if you ever pursue that avenue for property financing.

The annual mortgage payments are summarized on the “Returns Summary” tab.

Note: The DSCR calculation will always account for principal and interest, even if there is an interest-only term (as lenders traditionally calculate it).

Partial Assumable Seller Financing

The final (and likely rarest) scenario is if you assume the in-place mortgage on the property and take a seller carry. Again, ensuring the bank allows this and that a “due on sale clause” won’t be triggered when closing would be paramount.

Let’s say the seller is into the second year of ownership and has a 10-year bank loan with 24 months of interest only. You will assume the mortgage in month 16 (so there will be eight months of I/O remaining for you). The capital stack is still:

First Mortgage: 60%

Second Mortgage: 15%

Upfront Cash: 25%

The operations are struggling, and the seller will likely see negative cash flow once the interest-only period runs out. To entice you, they offer a 15% carry and are willing to match the terms of the 1st mortgage and take the lump sum balloon payment at the end of Year 10. Thankfully, the original loan originated in 2021, when interest rates were at historical lows.

Bank loan and seller financing assumptions look like this:

The annual mortgage payments are summarized on the “Returns Summary” tab.

You can see above that the principal payments will ramp up in Year 2 once the bank’s interest-only period ends.

Summarizing Seller Financing

We’ve covered three seller financing scenarios in the Multifamily Value-Add Model. Our Free Multifamily Template can also handle the financing scenarios in this post.

As rates remain elevated, traditional mortgages may be less feasible thanks to higher monthly expenses and fewer loan proceeds. Projects once prime for a conventional mortgage loan may no longer qualify, and creative financing measures are necessary to close a deal.

Savvy real estate investors looking to find and close deals in a challenging economic environment may suggest partial or complete seller financing to the existing owner. This could be the pathway to ensuring a real estate transaction closes.