Comparing DSCR, LTV, Debt Yield & Loan Constant

This week's article compares and contrasts four primary debt metrics commonly used when evaluating financed commercial real estate. Each metric serves a unique purpose to help assess risk from the perspective of lenders and investors.

Contents

Debt Metrics Quick Definitions

1. Debt Service Coverage Ratio (DSCR)

The DSCR looks at the net operation income ratio to debt payments.

DSCR = Annual NOI / Annual Debt Service

The higher the DSCR, the "safer" the investment.

2. Loan-to-Value (LTV)

The LTV looks at the allocation of loan proceeds to the total purchase price of the project.

LTV = Loan Proceeds / Purchase Price

The higher the LTV, the riskier the loan.

3. Debt Yield

The debt yield looks at the property NOI compared to the outstanding loan amount.

Debt Yield = Annual NOI / Outstanding Mortgage

A higher debt yield signifies a less risky loan amount.

4. Loan Constant

The loan constant takes the total debt service burden as a percentage of loan proceeds outstanding.

Loan Constant = Annual Debt Service* / Loan Balance

*Principal & Interest

A higher loan constant is indicative of riskier financing.

Debt Coverage & LTV Relationship

Debt service coverage ratio (DSCR) and loan-to-value (LTV) are a packaged deal. You can't talk about one without the other. That's because a lender usually makes a financing quote in LTV terms with the caveat that the property meets specific DSCR criteria.

DSCR Example

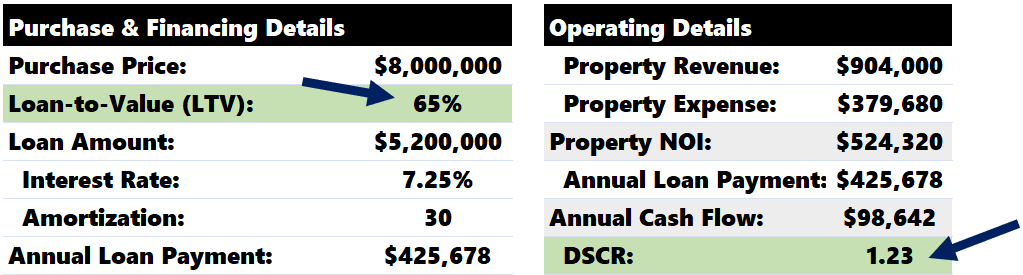

Let's take a property that is for sale for $8,000,000. The lender's original quote is a 70% LTV loan, but the property must hit a 1.20x DSCR.

Here are the loan terms:

70% LTV x $8,000,000 = $5,600,000 in total loan proceeds.

The annual debt service payment is $458,422.

Let's look at the property financials and focus on the DSCR.

Unfortunately, the property doesn't meet the lender's DSCR criteria 1.20. The DSCR is only 1.14x

$524,320 / $458,422 = 1.14

To get to a 1.20 DSCR, we'll need to back off the LTV. Let's try 65% instead of 70%.

With a 65% LTV loan, our annual debt service burden is lower, and the DSCR increases to 1.23, which is sufficient for the lender.

Unfortunately, this means we'd get $400,000 less in loan proceeds from the original 70% LTV quote, and we'd need to fund that with cash or some other creative route (such as preferred equity or mezzanine debt).

Debt Yield vs. DSCR & LTV

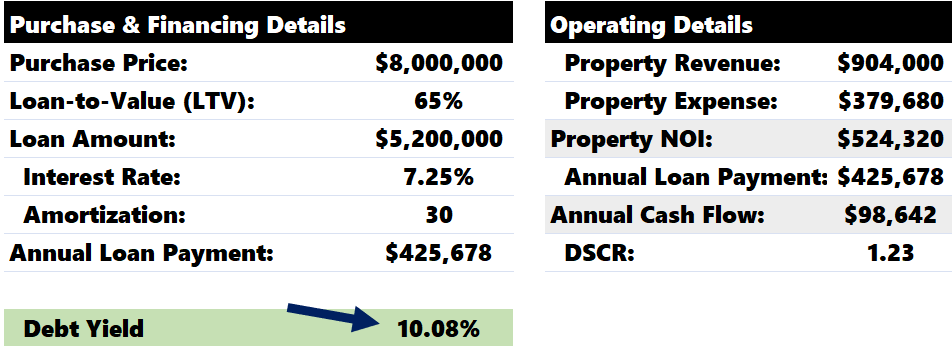

One extra layer of security a lender may require is that the project exceeds a debt yield threshold.

The debt yield tells a lender, if the borrower were to default and the lender took back the property, what would their annual return look like:

NOI / Outstanding Loan

A higher debt yield means the lender would get paid back sooner. When we calculate the debt yield in our sample scenario, we get 10.08%.

$524,320 / $5,200,000 = 10.08%

If the borrower defaulted on Day 1, the lender could expect to get paid back in about ten years (10.08% x 10).

Let's say the same lender from our first scenario, requiring a 1.20x DSCR, also requires an 11% debt yield. We'd need to return to our LTV assumption and lower it further.

A 59% LTV boosts the debt yield to 11.11%. Loan proceeds have fallen to $4,720,000. DSCR climbed to 1.36.

Related: We have an entire article on calculating and understanding the debt yield for further learning.

Loan Constant vs. Cap Rate

We've seen thus far how the LTV, DSCR, and debt yield all tie together. Increasing or decreasing the LTV assumption will directly impact the DSCR and debt yield.

The loan constant is on an island. As a refresh, the formula is:

Annual Loan Payment / Total Loan Amount Outstanding

When we change the LTV assumption, the loan constant won't be affected because the numerator and denominator change commensurately. The loan's interest rate and amortization period will impact the loan constant.

Generally speaking, a higher loan constant is riskier for the borrower.

We can calculate the loan constant from our current set of numbers.

$386,385 / $4,720,000 = 8.19%

This number on its own means a little. It is a lot more valuable if we compare it to the cap rate of the project. Let's do a cap rate calculation:

Cap Rate = $524,320 / $8,000,000 = 6.55%

The loan constant is considerably higher than the cap rate.

8.19% > 6.55%

What does this mean? The project has negative leverage. The financing is hurting your annual return. Yield will be higher if you purchase with 100% cash.

We can see this if we calculate a cash-on-cash return:

Cash-on-Cash = $137,935 / ($8,000,000 - $4,720,000) = 4.21%

The cap rate must be greater than the loan constant to benefit from leverage. We can play with the purchase price to find the pricing where:

Cap Rate = Loan Constant

When we do, the cash-on-cash return would also fall in line at 8.19%.

Summarizing the image above, with the current financing terms and operating data, as long as the price is below $6,403,000, leverage will be positive and boost investor returns (cash-on-cash).

Video: DSCR, LTV, Debt Yield, Loan Constant

Summarizing DSCR, LTV, Debt Yield & Loan Constant

The formulas for the four primary debt metrics are relatively straightforward.

DSCR = NOI / Debt Service

LTV = Loan Proceeds / Purchase Price

LTC = Loan Proceeds / (Purchase Price + Repairs/CAPEX)

Debt Yield = NOI / Loan Proceeds Outstanding

Loan Constant = Debt Service / Loan Proceeds Outstanding

The purpose of each is also essential and plays a role in every financed real estate deal:

DSCR: Measures the clearance property income has over the loan payments

LTV/LTC: Tells us what percentage of the capital stack constitutes debt

Debt Yield: Calculates the property's yield on outstanding debt

Loan Constant: Shows us the debt service as a percentage of the outstanding debt

Using real numbers, we saw how these four metrics interact and how we can use them to improve the overall analysis of the investment’s financing options.