Multifamily Development with HUD: Underwriting BSPRA

If you're a for-profit multifamily developer considering FHA for your financing, you may benefit by taking advantage of the BSPRA credit.

Contents

Disclaimer: You should verify with your lender, equity partners, attorney, and accountant how to correctly account for BSPRA. This article is purely theoretical, and slightly different circumstances could significantly alter the impacts on project-level returns, partnership returns, and taxes. My interpretation may not be accurate for every scenario.

BSPRA Credit Primer

The builder sponsor profit and risk allowance (BSPRA) credit allows you to tack on an additional "paper cost" to the total construction when using HUD 221(d)(4) financing.

Specifically, you can add up to 10% of the replacement cost (must exclude the land cost) and get loan proceeds for that additional expenditure. You'll effectively see more leverage and less cash equity.

The BSPRA paper credit can be hard to conceptualize, so let's look at actual sources and uses statements with and without BSPRA.

BSPRA Sources & Uses Example

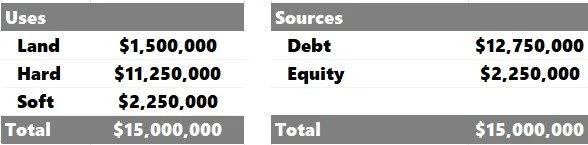

One of the biggest perks of using HUD 221(d)(4) is the potential for more leverage, perhaps as high as 85% LTC on market-rate. If we looked at a $15,000,000 project with an 85% construction loan:

The developer needs $2,250,000 in cash (or 15% of total construction costs).

Let's run another example with a BSPRA credit. The developer could get up to a 10% cost increase for hard/soft costs.

($11,250,00 + $2,250,00) * 10% = $1,350,000

On the Sources side, there's also an offsetting credit. Now the cash equity required is only $1,102,500, about half of what was needed in our scenario without BSPRA.

Although the total construction cost went from $15,000,000 to $16,350,000, the cash burden is less for the developer.

Important: The lender would also scrutinize your development proforma to ensure the stabilized NOI is sufficient to cover the increased financing cost related to the BSPRA adjustment. If this isn't the case, and the DSCR falls below an acceptable threshold, you wouldn't be eligible for the full credit.

Remember, while the BSPRA helps you bring less cash to the closing table, it also increases total loan proceeds, affecting your fixed loan payment once your loan begins amortizing.

BSPRA Eligibility

There are some rules when using BSPRA (open as a PDF document) for market-rate development:

A developer fee isn't allowed as a mortgageable cost (pg. 57 section “BB” of the link above)

The builder's profit isn't permitted as a mortgageable cost (pg. 63 section “N” of the link above)

Note: While the link above is dated (2016), it was the only source that I could link. The more recent literature was Word docs with no direct URL.

The premise of the BSPRA credit is that the builder (it can be a third-party fee-based contractor or a related entity to the developer) will take an equity position in the project instead of charging the developer their profitability fee and share the project's upside potential. Ultimately, the developer and the general contractor would negotiate the specific terms.

As I mentioned earlier, you can apply the BSPRA credit to most expenses, but you must exclude land. Per HUD’s Multifamily Accelerated Processing Guide (opens as a PDF document), some other expenses NOT included are:

Land/hold costs

Off-site work

Payment for acquisition of leasehold

Ground-rent

Relocation expense

Supplemental management funds

Major moveable equipment

See page 391 from the link above for more information.

Benefits of BSPRA

Higher Leverage

There's potential to take an already high leverage threshold (compared to other construction loan products), ramp it up even higher, and boost returns on investors' cash.

Alignment

Giving the GC a minority equity stake creates more alignment. It could motivate them to hit key deadlines, stay on budget, and build a superior project that could maximize investment returns.

Flexibility

For developers that are also the GC, creating an agreement between the developer and the GC entity would be seamless.

General HUD Financing Terms

Higher leverage, longer amortization periods, non-recourse, and "assumability" for a future buyer make HUD financing appealing. HUD rates have been historically lower than other traditional bank/construction loan products.

Drawbacks of BSPRA

Higher Debt Service

As we just discussed, getting a BSPRA credit increases total loan proceeds, equating to a more expensive monthly debt payment once the loan term begins amortizing, making the project more risky.

If the quoted interest rate and MIP are 6.5% with a 40-year amortization schedule, the monthly debt service in each of the two scenarios is the following:

Loan of $12,750,000: $75,112

Loan of $13,897,500 (with BSPRA): $81,872

That would be $81,120 in annual debt service in the BSPRA scenario.

Note: Other construction loan products may only offer floating (variable) rate options. HUD is a fixed rate.

No Developer Fee

While the BSPRA may help negate the lack of development fee on a market-rate project, it's not a perfect substitute.

Builder Disinterest

Your builder must be onboard with deferring a profit for future project upside. Delaying a fee is risky and could limit groups' interest in building your project.

General HUD Financing Terms

While there are some great perks of using HUD, there are other drawbacks, including:

Longer timelines

More oversight/compliance/audits

More 3rd party costs/reserve requirements/MIP

Video: Underwriting BSPRA in Tactica's Development Model

Other Resource: I found an incredibly insightful and succinct video from Kyle Jean with Bedford Lending on the BSPRA credit. If video learning is preferred over thumbing through a 400-page document from HUD, give it a view! He really knows the ins and outs of HUD and BSPRA.

Developer & Builder Partnership

A developer and builder can structure their partnership in many different ways that will ultimately come down to internal negotiations. I recently wrote an article about a land contribution in multifamily development and how the land contributor may look for an equity stake in the project instead of taking payment of cash for the land.

While the circumstances are slightly different, how the partnership is structured could be very similar in a BSPRA scenario.

Summarizing BSPRA

HUD 221(d)(4) financing is a unique financing option that for-profit developers can use that offers some major benefits, including:

Lower interest rates

Longer amortization terms

Higher leverage

Non-Recourse

Future Assumability

There are costs, compliance, and longer timelines related to HUD that you'd need to way against other financing options. You're also not allowed to charge a development fee or pay

The BSPRA credit can help improve an already solid HUD financing program, specifically allowing for a "paper cost" of 10% of construction costs and a credit to the developer to help reduce their cash requirement at closing.

Benefits of BSPRA include the following:

Higher Leverage

Better developer/builder alignment

The flexibility of Developers doubling as GC

Perks of the general HUD financing terms

Drawbacks of BSPRA include the following:

Higher stabilized debt service

No developer fee

Potential for builder disinterest

Detriments of general HUD financing terms

Ultimately, HUD 221(d)(4) financing, in tandem with the BSPRA credit, can offer developers a distinctive funding solution to finance a ground-up construction project if the program fits the developer’s and builder’s preferences.