A Guide to Underwriting Multifamily Property Tax

When analyzing an investment opportunity, I argue that property taxes on multifamily homes are the most critical expense line item. In many parts of the country, real estate taxes will be the most considerable expense as a percentage of property revenue.

When analyzing a property, I’ve always devoted an entire Excel tab to real estate taxes. I have been fortunate to work on projects spanning various submarkets. Although all states will have slightly different tax calendars and nuances, the big-picture exercise is always the same when underwriting property tax: Understanding the future property tax exposure.

Property Taxes on Multifamily Homes Primer

Investigating Public Data

There is much investigation that needs to take place on the front end. This exercise typically involves going on the county website of your subject property and pulling historical tax statements. You are looking for past property assessments, tax bills, special assessments, payment timing info, and discounts.

Property Assessment

The county's property valuation calculates the ad valorem tax bill. How often this valuation is updated will depend on the county. In my neck of the woods, it is annually.

Tax Bill

The tax bill will indicate how much the property owner pays in a given year. I will not get into the weeds on how this number is determined. That could be its article. Property classification, school referendums, public services, and other state, county, and city budgetary provisions heavily influence it.

Special Assessment

Occasionally, the property will be on the hook to pay for public projects levied for a particular area. These projects include sidewalk repairs, road construction, sewer improvements, and recycling services.

Note: If a property is responsible for a special assessment, while it is technically part of the tax bill, I will separate this portion of the expense to understand the "true" property tax net of any temporary special assessment.

Payment Timing

Every state will have different requirements for when payments are due each year. Some states will require one payment; some will offer multiple payment windows throughout the year.

Discounts

Some states will offer a discount if property owners pay 100% of their property taxes upfront instead of spreading out the yearly payments.

You can find all of the above information online. County websites will look different and have a much different user experience, but property data is public information everyone can access.

Forecasting

The unknowns are the items we need to estimate in the proforma underwriting. There are things like:

Reassessment Post-Sale

Reassessment Timing

Assessment Increases Post-Sale

Applicable Tax Rate

Reassessment Post-Sale

If you pay more for a property than it is currently assessed at, will the Assessor raise the assessment significantly? An apartment property is estimated at $10,000,000, and the broker says pricing guidance is $15,000,000. The current applicable tax rate is 2%, meaning that the current year's taxes payable are $200,000.

What would happen if you paid $15,000,000 for the property? Most astute investors will talk about this post-sale reassessment in terms of the "percentage of the purchase price." In South Florida, it's common knowledge that this increase is 80% - 85% of the purchase price. In Minnesota, 90% – 95% of the purchase price is commonplace in the Twin Cities metro.

If this was Minnesota, and I underwrote a 95% post-sale reassessment, the property's assessment would increase to $14,250,000. Assuming the applicable tax rate held steady at 2%, taxes payable would increase to $285,000.

$14,250,000 x 2% = $285,000

That is $85,000 more than the property tax expense in the historical financials. That is a lot of NOI that could be lost if you were to pay a total of $15,000,000.

Reassessment Timing

If taxes are going to increase, when will it happen? One year from now? Two years? It can be helpful for investors if this is pushed back as far as possible, especially if ownership plans to do an extensive value-add. The cash flow from those early renovations can help hedge the future tax increase.

The timing of this increase will also have to do with the tax calendar of the taxing jurisdiction. Depending on when you close during the year could impact when increased taxes officially hit the proforma.

Assessment Increases Post-Sale

Once you've determined when the most impactful reassessment will occur and for how much, you will need to estimate what the assessment increases (or decreases) will ensue after that.

Applicable Tax Rate

If the tax rate is 2% this year, what will it be next year? Has the rate been increasing or decreasing over the years? Most investors hold the most current applicable tax rate steady for the entire investment hold. I have seen conservative underwriting that may increase it by a couple of basis points each year.

Multifamily Property Tax Forecasting Case Study

In our free multifamily underwriting template, Value-Add Model, and Redevelopment Model, I give investors control over all the knowns and unknowns. While I can't tell you how to underwrite real estate taxes in your submarket, the underwriting tool can harness your knowledge base and create a real estate tax estimate encompassing all the essential pieces.

Related: Underwriting property taxes in a development proforma requires a slightly different mindset and is beyond what this article will cover.

Gathering Public Data

I will walk you through how I find pertinent real estate tax information on an apartment deal. I picked a random multifamily property. Typically, you would search the county website for a property by its parcel ID or address. More sophisticated county websites will have a map function you can use to find the property.

The first thing I want to do is to gather all the historical tax information. For this particular property, the data goes back to 2016. To save time, I will start in 2019.

Note: In Minnesota and many other states, property taxes are paid one year in arrears. This means your current year's property tax bill is based on the prior year's assessment. In other words, when property valuations are finalized in April of each year and mailed to owners, the property tax paid on this assessment will not be due until the following year.

Since I started in 2019, the 2018 assessment would determine the 2019 property tax calculation. The appropriate years would be the first inputs you would need to enter.

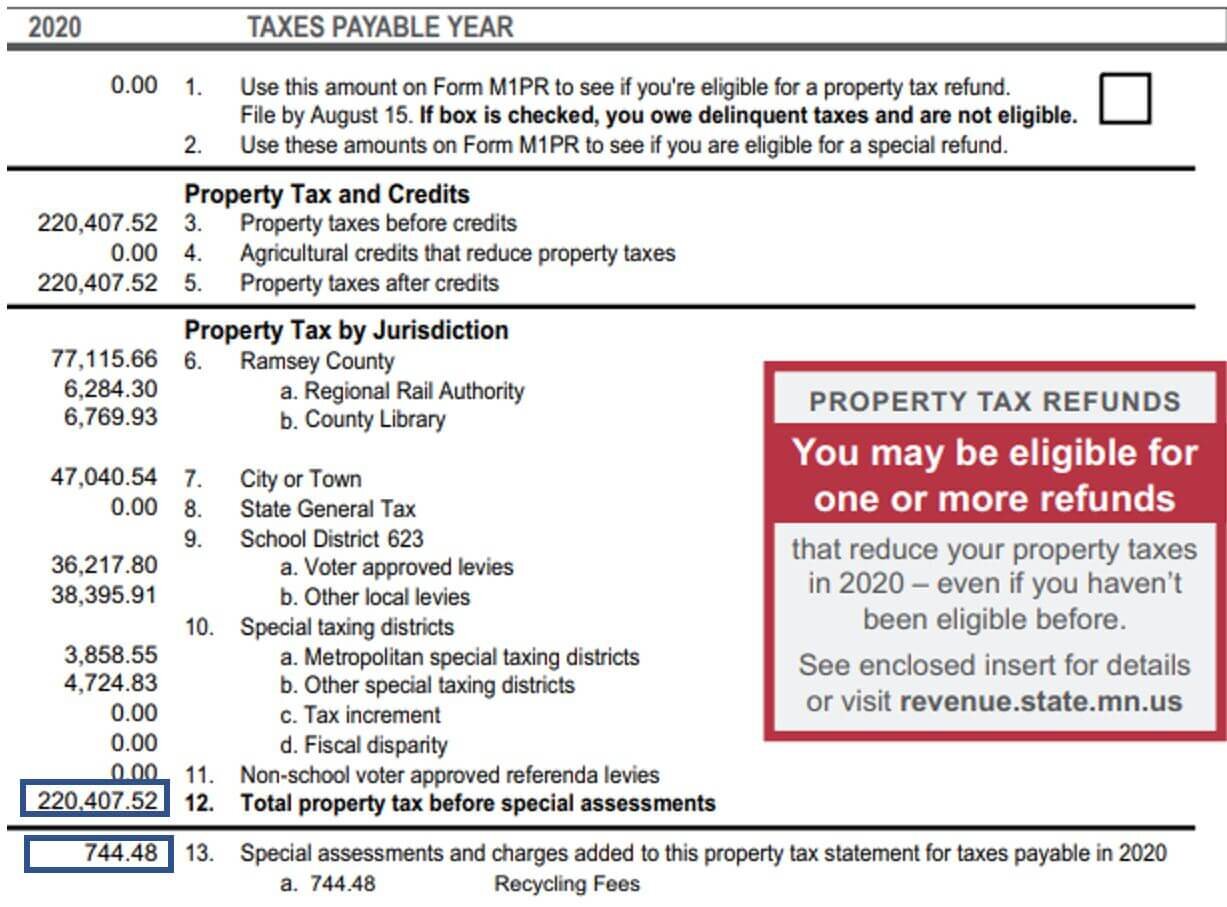

Now, we need to get the 2018 assessment and 2019 payable amount. I opened up the tax statement, and I am focusing on the following:

For the 2019 taxes owed, the value was set in 2018. This can be a little confusing. It may seem like I should be grabbing the $10,000,000 from above. That is not the case, however. The 2018 assessment is in the 2019 column and is $12,457,200. The "2018 Values for Taxes Payable in 2019" header assures that this is the correct course of action.

The next part is grabbing the taxes payable.

I want the total property tax before the special assessment. While the special assessment is essential, and we will record it, I will grab that separately. We can fill out all the relevant information for the 2019 tax year with this information.

Note: There is no discount for paying property tax early in MN. In states that there are, this is usually stated as a "percentage of total taxes payable, and generally ranges between 2% - 5%.

The tax rate will be calculated automatically (Payable / Assessment Amount) along with the Net Payable (Payable + Special Assessment)

I would follow the same steps as before for the 2020 tax year.

The assessment in 2019 for 2020 payable is $12,830,900. The previous year was the amount we just entered in the last step (it's an excellent verification).

Taxes payable data looks the same as before. Remember to grab the special assessment.

And then, we need to enter this into the model.

There are already insights to be gleaned here. The applicable tax rate is dropping! Hopefully, that trend will continue. The special assessment also dropped considerably. It would be wise to figure out why. I’m not afraid to call the local assessor and pick their brain. They are pretty helpful, especially when I am working in a state that I am unfamiliar with.

As of writing, it is April 8th. While we do not know the taxes payable for 2021, we can make a reasonable guess because the 2020 assessment is finalized on the county website. That will be the final piece of "known" information available to use.

Wow, a massive jump in the assessment!

Because there was no "Payable" amount entered in 2020/2021, the model will estimate the “Net Payable” by multiplying the current year's applicable tax rate by the assessment amount:

$18,406,300 x 1.72% = $316,182

This method tends to be the industry standard. While we hope the tax rate drops again, it's best to be conservative and use the current rate. It is up to you to enter a special assessment and discount. I will also hold the 2020 special assessment steady ($744).

Before considering a sale'ssale'st on future taxes, we know that taxes will jump nearly $100,000 in 2021.

Now, we must begin thinking through the unknowns.

How To Forecast Property Taxes

The broker's pricing guidance on this particular community is $25,000,000. The big questions are:

At what percentage of the pricing guidance will this property likely be reassessed?

What year will this probably happen?

What will happen to taxes payable after the reassessment post-sale?

As I mentioned earlier, this reassessment is usually 90% - 95% of the sales price in the Twin Cities. If this were in Duluth or some other tertiary city, I would likely scale this back to 80% - 85%. It will depend on how much sales velocity there is and an understanding of what has happened to other properties’ assessment upon sale. Looking at tax comps is a great idea to gauge how the assessor has handled valuing other recent sales.

I have analyzed properties in the Dakotas and don't underwrite any assessment growth even when the proposed sales price is 100% above the assessment level. This is because there is not nearly enough sales volume for the assessment community to justify one sale as "the market assessment."

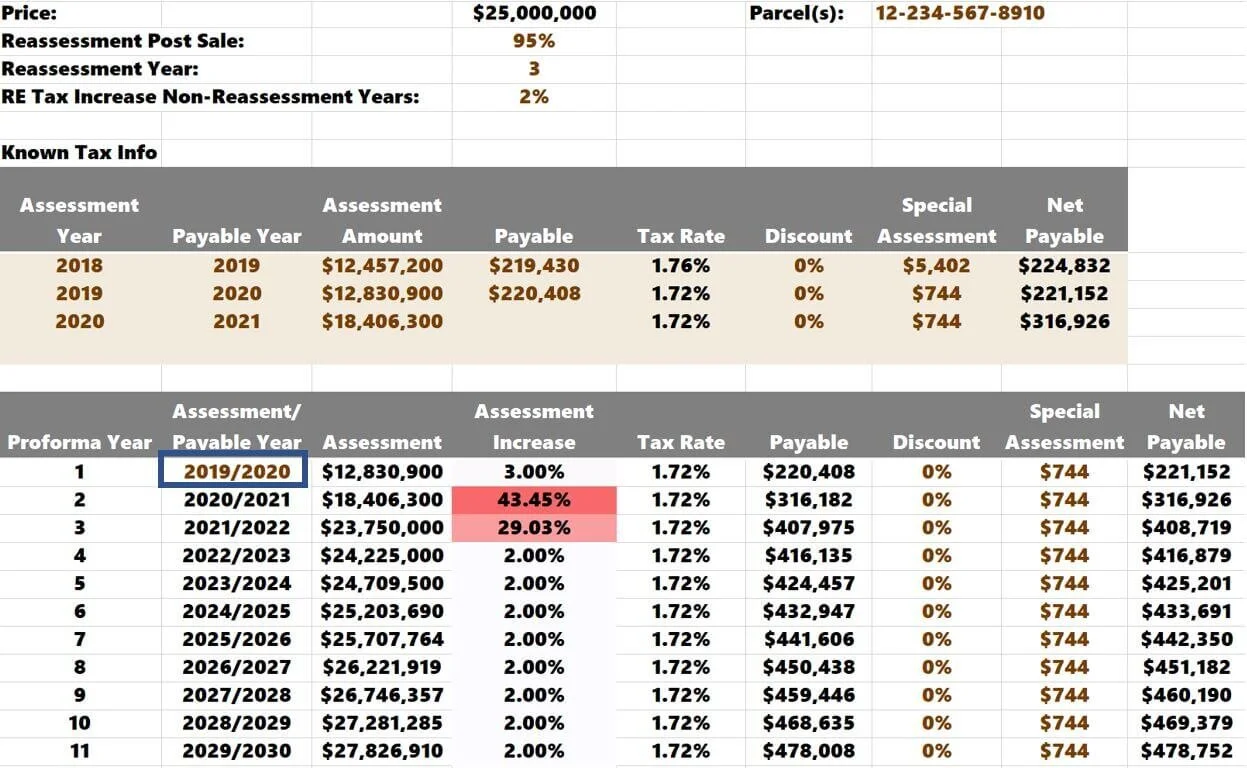

I will assume a 95% reassessment in Year 3 for this particular deal. If this property closed during the summer of 2020, the sale would first be detected in 2021 (for 2022 payable). Remember, we already have an accurate idea of what 2021's taxes will be (Year 2).

After this reassessment, I will assume that taxes continue to increase by 2% annually for the duration of the proforma.

The final step is determining which year Proforma Year 1 will officially begin.

There will be a drop-down in the highlighted cell above where you can select which year you want to be Year 1 of the proforma. There is significant exposure next year and after the property is reassessed, factoring in the sales price of $25,000,000.

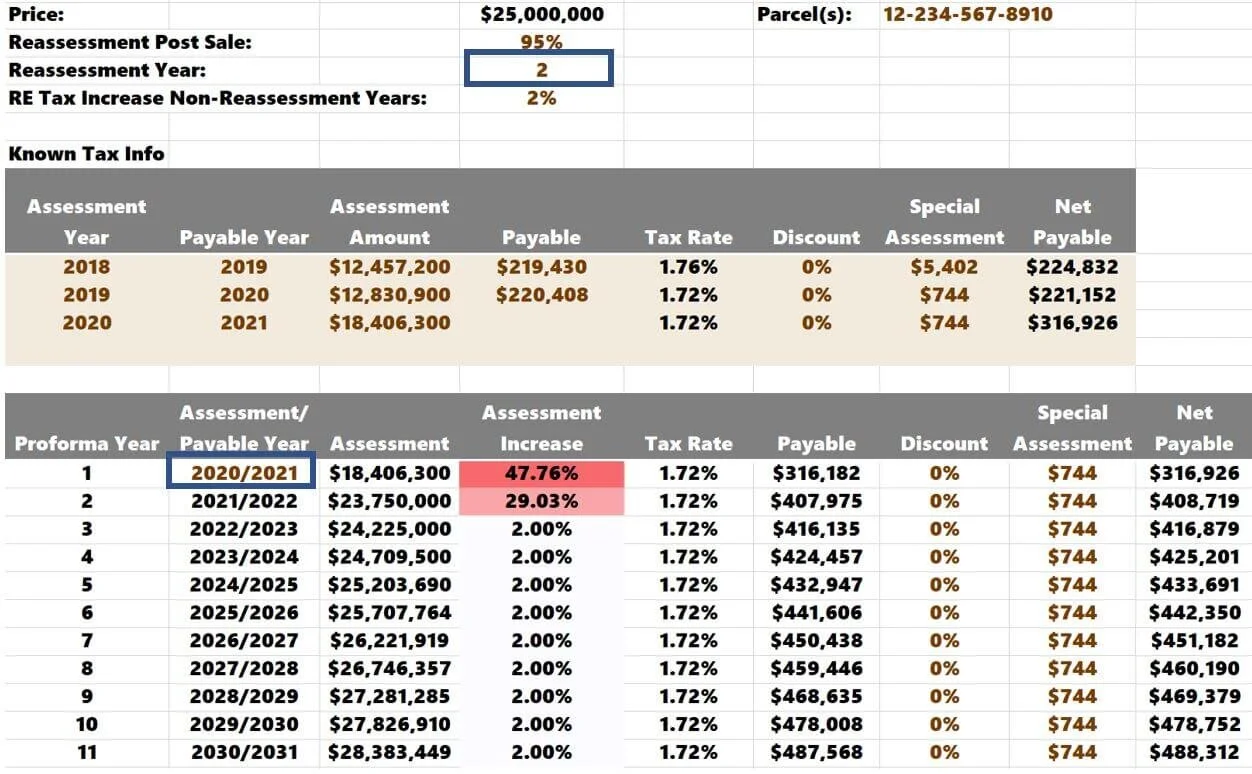

If you want to be extra conservative, you could start your tax year as 2020/2021 and change the Reassessment Year = 2.

Taxes will now ramp up instantly.

The Discount and Special Assessment columns are brown text because you can overwrite them. However, they do tie to the "known" data above.

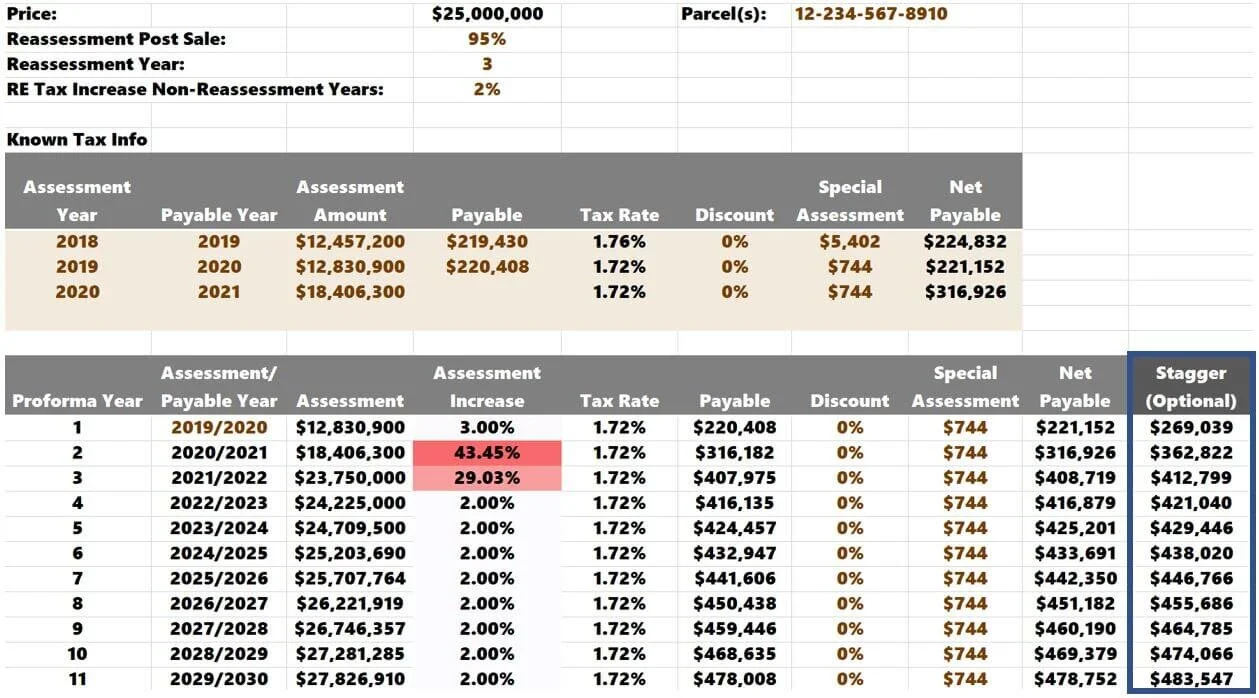

Advanced Tip: In the Value-Add and Redevelopment Models, I rolled out a "Stagger Option." You can use this when the tax year doesn't align perfectly with the proforma year.

Example: Property taxes are paid in May and October in MN. For this property, we are assuming a summer sale. The timing of this sale would mean that Year 1 of the proforma would be compromised of 50% of 2020 taxes (October 2020 payment) and 50% of 2021 taxes (May 2021 payment).

The taxes can align perfectly with the proforma by utilizing the stagger feature:

Year 1 Tax = $221,152 / 2 + $316,926 / 2 = $269,039

Year 2 Tax = $316,926 / 2 + $407,975 / 2 = $362,822

The stagger would not be necessary if you were expecting the sale to close in November 2020. The current owner would make both 2020 tax payments, and your Year 1 tax payment would be the 2021 taxes payable.

The stagger option is helpful because it's accurate but doesn't have a material effect on investment returns. In other words, if the proforma doesn't align perfectly with the tax calendar, don't fret about it. Ensure you are conservative with your reassessment assumption and understand the future tax liability.

Summarizing Property Taxes on Multifamily Homes

When developing the multifamily financial model, real estate tax underwriting was one of the most challenging components to build. It has taken much repetition working in various submarkets to feel confident in a tool that can handle the multiple tax calendars and subtle discrepancies between the states.

By focusing on gathering public data followed by forecasting, I am confident that this tool will give investors an accurate estimate of future property tax liability in their proforma underwriting. It is still up to the investor to research the submarket and understand the tax calendar, sales velocity, and the assessor's general practices.